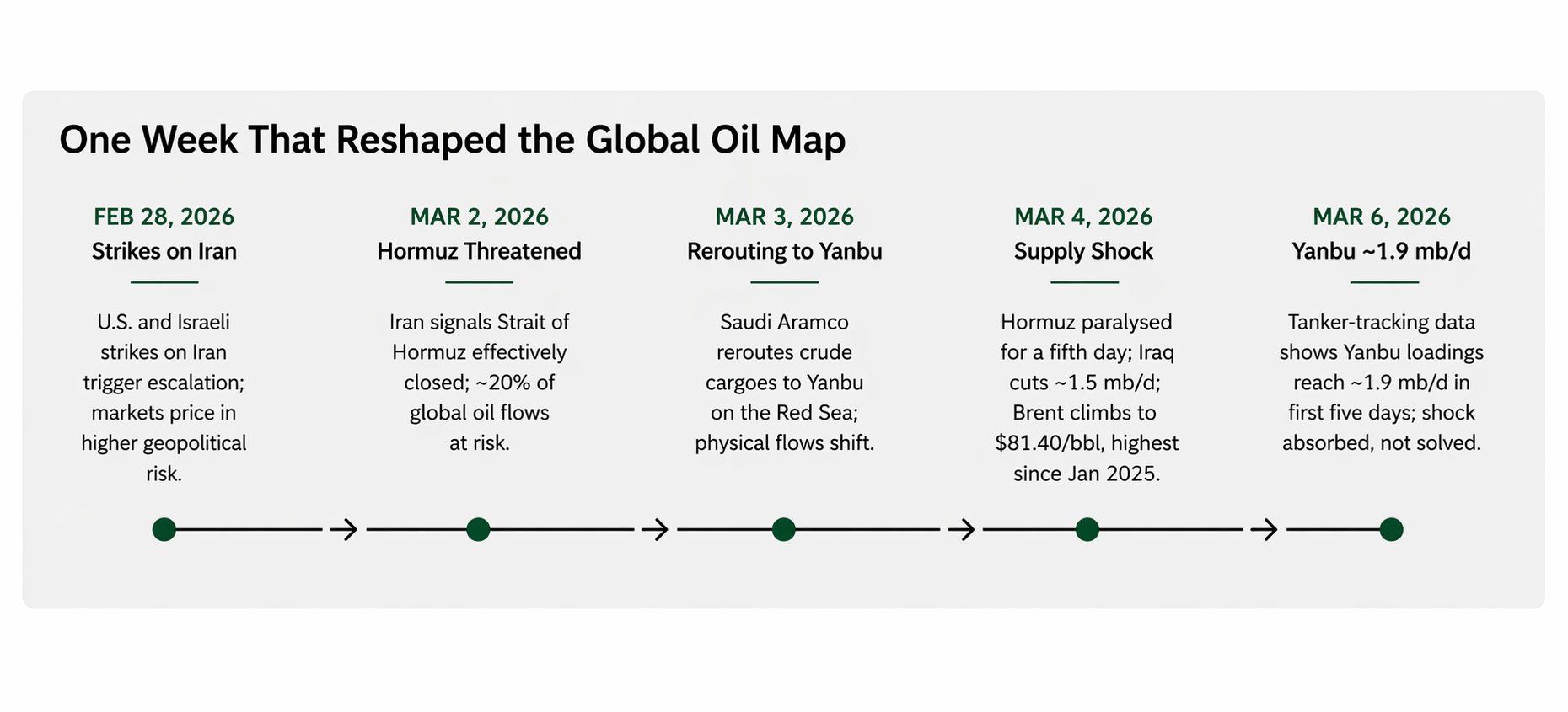

Middle East Conflicts Send Oils into Turmoil

After joint U.S. and Israeli strikes on Iran and Tehran's retaliation, Gulf export flows were slowed, forcing Saudi Arabia to reroute crude exports westward to Yanbu, an industrial hub, on the Red Sea instead. That makes this a strong and interesting case to look at because it shows a direct chain from military escalation to shipping disruption, rerouted barrels, tighter prompt supply, and higher crude and gas transport costs. Since roughly 20% of global petroleum liquids consumption normally passes through Hormuz, any sustained disruption there rapidly feeds into global commodity pricing.

Yanbu Emerges as Saudi Arabia's Back Up Oil Route

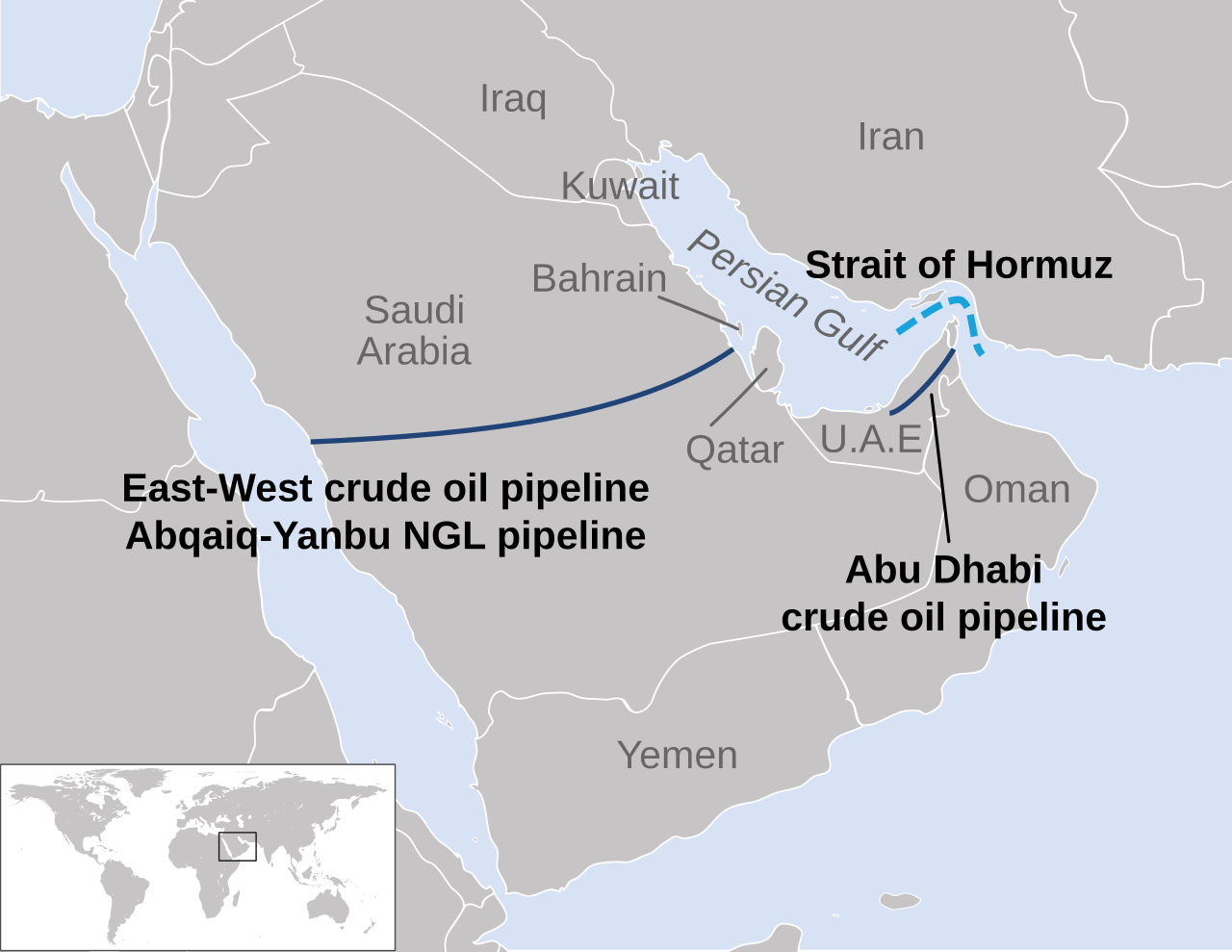

Yanbu's rise to 1.9 million barrels per day in the first five days of March matters because it shows Saudi Arabia has a backup route when the Strait of Hormuz is disrupted. Normally, a large share of Saudi oil leaves from ports on the Gulf and passes through Hormuz, so when that route became unsafe, Saudi Arabia turned to the East-West pipeline, a major pipeline that carries crude across Saudi Arabia from its eastern oil fields to the Red Sea port of Yanbu in the west.

Instead of sending oil out through the Gulf and into a conflict-exposed chokepoint, Saudi Arabia can move some of it across land and export it from the other side of the country. That helps explain why Yanbu loadings rose from 1.1 million bpd in February and 1.3 million bpd in January to 1.9 million bpd in early March.

But the numbers also show the limits of this solution. Saudi Arabia still exports more than 7 million bpd, with roughly 6 million bpd usually moving through Hormuz, so even a strong increase at Yanbu only replaces part of its normal Gulf flows. In theory, the East-West pipeline can carry up to 5 million bpd, and has reportedly been expanded higher before, but in practice Yanbu rarely loads more than 2.5 million bpd. That means the real constraint is not just the pipeline itself, but how much oil the port can actually handle and load onto tankers.

The key point is simple: Saudi Arabia does have a real emergency workaround, which makes it more resilient than some of its neighbours, but it is still only a partial fix. It reduces the shock, but it does not remove it, which is why the market still sees this as a serious supply disruption rather than a problem that has already been solved.

Saudi Oil Detour Softens Supply Shock

Alternative infrastructure reduces the shock, but it does not eliminate it, because Saudi Arabia's fallback option is a partial bypass rather than a full replacement for Hormuz. The East-West pipeline lets crude move from the kingdom's eastern fields to Yanbu on the Red Sea, which is why Saudi Arabia is more resilient than Gulf producers with no meaningful alternative route; but the volumes still fall short of what normally moves through Hormuz, and Reuters notes Saudi still needs to reroute roughly 5-6 million bpd, while Yanbu itself has limited loading capacity and some tanker fixtures have already failed.

Even where the pipeline helps, the market still runs into physical bottlenecks at the export end: storage, berthing slots, tanker availability, and the practical difficulty of scaling Red Sea loadings fast enough to match Gulf flows. Just as importantly, the workaround does not remove geopolitical risk so much as move it westward. Instead of relying on Hormuz, more barrels become dependent on the Red Sea corridor, which still faces Houthi attack risk, while freight and insurance costs have surged sharply, with Reuters reporting Yanbu shipping rates more than doubled and war-risk premiums rising steeply as owners and insurers reprice exposure.

So the Saudi system buys time and softens the initial supply shock, but it cannot fully neutralise it: some barrels are delayed, some become more expensive to deliver, and the market is still left with pricing disruption because the alternative route is itself constrained and insecure.

The Limits of Saudi Arabia's Hormuz Bypass

The price action confirms that the market sees this as a front-end supply shock. The front of the curve tightened sharply: Reuters described a roughly $10 backwardation between front-month and six-month Brent. That structure suggests the market is pricing immediate scarcity and logistical stress, not yet a permanent long-run loss of productive capacity.

At the same time, disruptions in Middle East sour crude flows pushed heavy crude prices in the Americas, Europe and Africa to multi-year highs as refiners searched for substitutes. Brent crude, the international benchmark, has risen about 30% since the close of trading last Friday before the conflict began, climbing above $94 per barrel, The Caspian Post reports, citing foreign media. Meanwhile, the US benchmark West Texas Intermediate (WTI) crude has surged even more sharply, gaining around 37% and briefly crossing the $92 per barrel mark.

Saudi rerouting through Yanbu proves some resilience exists, but current pricing shows the market does not believe that resilience is enough to fully replace Hormuz flows. For commodities, that means stronger nearby crude prices, wider prompt backwardation, firmer heavy-sour differentials, and spillover into LNG shipping and gas logistics. In short, the Middle East war is now affecting energy markets through the most important channel possible: the physical movement of barrels.

Data Sources

- EIA — Strait of Hormuz oil transit chokepoint

- Reuters — Yanbu shipping rates double, Saudi diverts oil from Hormuz

- Reuters — Heavy crude prices hit multi year highs after Iran conflict disruption

- Reuters — Oil derivatives signal market sees Middle East shock as short lived

Disclaimer

This report is published by 6:05 Markets for informational purposes only and does not constitute financial advice, an offer to buy or sell securities, or an investment recommendation. The information contained herein has been obtained from sources believed to be reliable, but 6:05 Markets makes no representation as to its accuracy or completeness. Past performance is not indicative of future results. Readers should conduct their own research and consult with a qualified financial advisor before making any investment decisions. This report is intended for the named recipient only. Unauthorised reproduction or distribution — in whole or in part — is prohibited without the prior written consent of 6:05 Markets.

© 2026 6:05 Markets. All rights reserved. Website: 605Markets.com · Linkedin: https://www.linkedin.com/company/6-05-markets

Back to Energy Reports